Japanese Yen Fourth Quarter Recap

The anti-risk Japanese Yen had a mixed performance against its major peers throughout the fourth quarter of 2021. It weakened against haven-oriented currencies, such as the US Dollar and Swiss Franc. On the other hand, it found some strength against growth and cyclical-sensitive currencies such as the Australian, Canadian and New Zealand Dollars as volatility hit stocks.

Inflation and the Fed Remain the Focus in Q1 2022

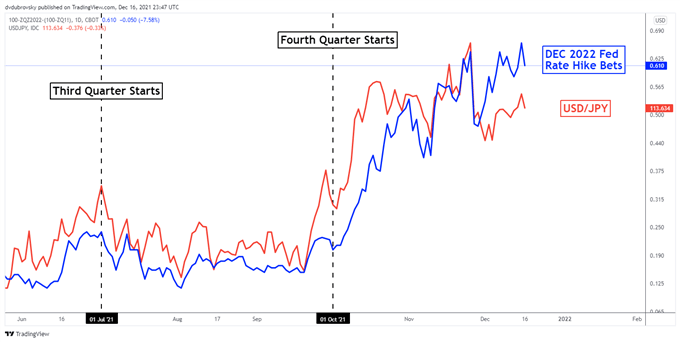

For USD/JPY, the road ahead in the first quarter of 2022 will likely remain heavily glued to market expectations of how hawkish the Federal Reserve will be – see chart below. In December, the central bank doubled the pace of tapering asset purchases, which will now see it end in early 2022. This will likely give the central bank maneuverability should it need to raise rates sooner than expected.

This will of course depend on how inflation evolves. Headline price growth is at its fastest pace in almost 40 years in the United States. Expectations are that price growth will remain above the central bank’s target next year, with Core PCE running around 2.7% in 2022. However, a key risk could come if inflation expectations become “de-anchored.”

December 2022 Fed Rate Hike Bets Vs. USD/JPY

Chart Created Using TradingView

The Labor Market May Keep the Fed on its Toes, Will USD/JPY Rise?

When inflation expectations are anchored, it typically means that short-term price growth does little to impact long-run estimates. This could be due to people expecting the Federal Reserve to maintain its inflation target down the road. However, if consumers anticipate inflation to linger instead, then those estimates can become “de-anchored”.

This can occur when workers, facing high inflation, demand higher wages to combat losing purchasing power. Businesses can respond by driving up costs of products to counter paying higher salaries. This creates a spiral — difficult for a central bank to counter. With that said, the Federal Reserve has ample room to tighten monetary policy given how loose policy has become in the post-Covid world.

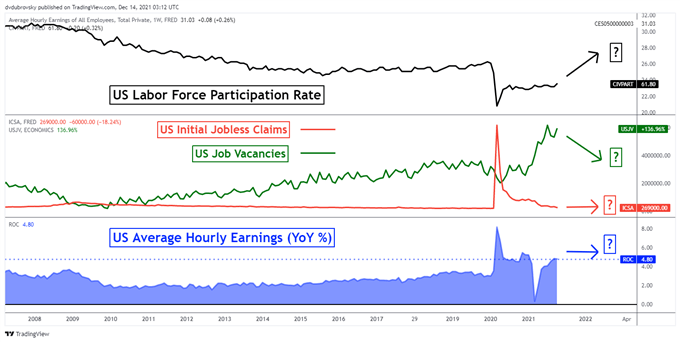

How does the US labor market look? As the chart below shows, the labor force participation rate remains stubbornly below pre-Covid levels. This is despite the country recovering about 80% of jobs lost since the Covid shock in 2020. On the plus side, jobless claims are at their lowest since 1969 while the number of openings is at their highest on record.

These trends hint that the country might be able to accommodate a surge in labor force participation without bringing up unemployment too quickly. If new workers entering the labor force seek higher wages amid elevated inflation, then salaries could rise, pushing up prices and opening the door to a more hawkish Fed. That could keep the focus for USD/JPY tilted upward. Another consequence might be more stock market volatility. This is something the JPY may capitalize against AUD, CAD and NZD.

Watching the US Labor Market in 2022

Chart Created Using TradingView